BoardMemo #2: Import Shock — How 2025 Tariffs Are Reshaping Strategic Positioning in the U.S. Auto Market

Why domestic production, supply chain localization, and import exposure now define competitive advantage

Effective April 2, 2025, a 25% U.S. tariff on imported vehicles and auto parts will go into effect, marking a pivotal shift in trade policy. While positioned as a move to bolster U.S. manufacturing, the immediate fallout will be inflationary, industry-disruptive, and highly uneven. Automakers with deep U.S. footprints are poised to benefit or suffer less, while import-reliant players face significant margin pressure, market share losses, or exit threats. Expect higher consumer prices, a shift in model mix, a boost to used cars, and potential long-term restructuring of supply chains.

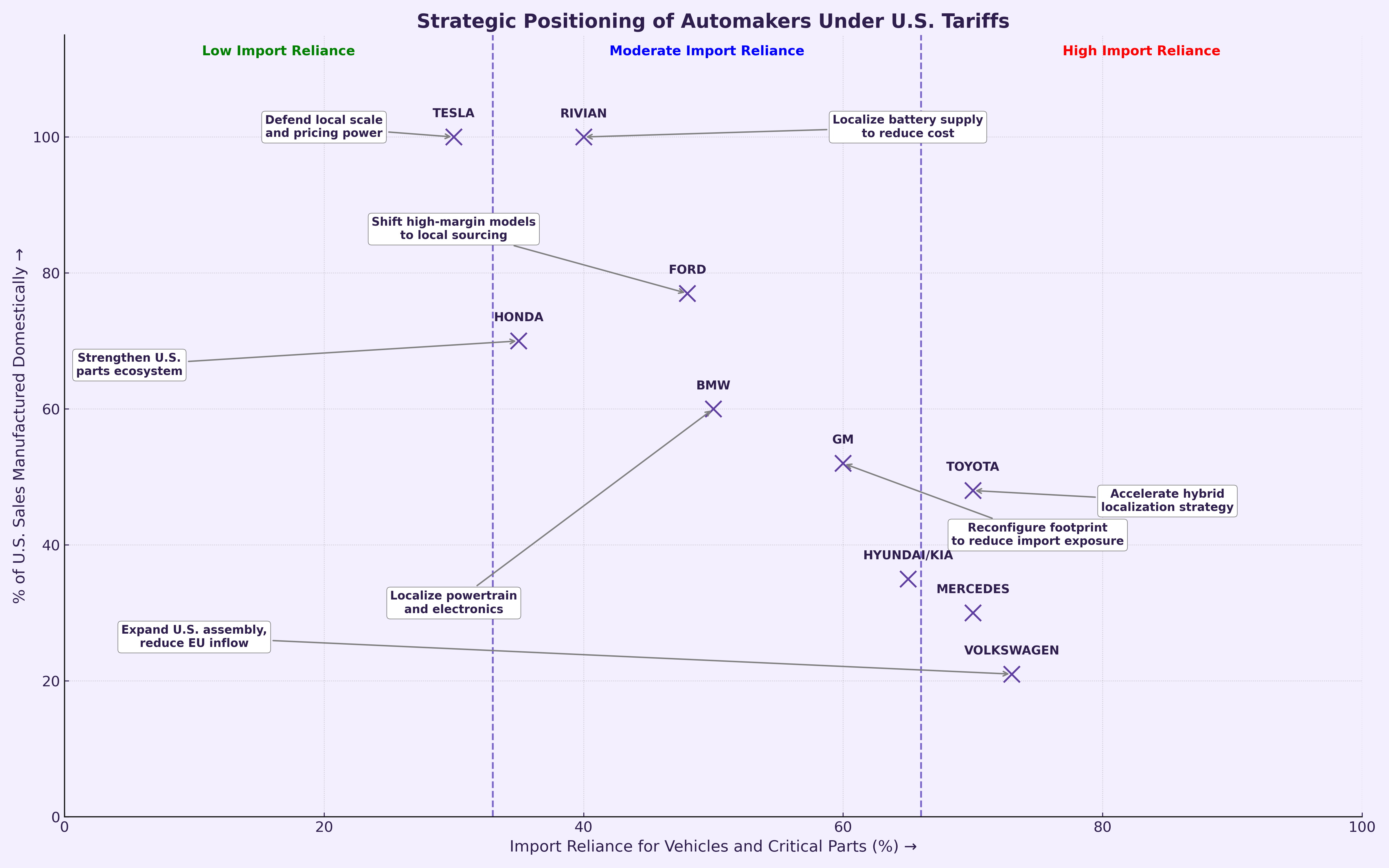

Automakers Strategic Positioning Under Tariffs

Two key factors define strategic positioning:

X-axis: Import Reliance for Vehicles and Critical Parts

Y-axis: % of U.S. Sales Manufactured Domestically

This creates three practical strategic zones:

Localized Advantage: High U.S. production, low import reliance (e.g., Tesla, Rivian)

Strategic Risk Management: High U.S. production but significant import reliance (e.g., Ford, GM)

High Exposure: Low U.S. production, high import reliance (e.g., VW, Toyota, Mercedes-Benz)

Key Insights

Tariffs = Tax: A 25% tariff is expected to add $6,000+ to prices of import-heavy models. The cost will fall on both consumers and import-centric OEMs.

Tesla & Rivian: Virtually 100% of their U.S. sales are domestically built, with relatively low imported content. Tesla still imports ~30–40% of its components, but its vertically integrated model shields it from major exposure. Rivian needs to localize battery supply to reduce cost

Ford: ~77% of U.S. sales are domestically produced. Remaining 23% are imports, mostly from Mexico/Canada. Strong domestic footprint, but part supply chain remains global.

GM: Only ~52% of U.S. sales are domestically produced. Nearly half are imports—30% from NAFTA, 18% from overseas. Exposure is high, requiring a footprint rethink.

Toyota: ~48% of U.S. sales are built in the U.S., 27% in NAFTA, 25% overseas. Import-heavy, especially on Lexus and hybrids. Many U.S.-built Toyotas also have high foreign parts content.

Honda: ~70% of U.S. sales are built in the U.S., with most imports from NAFTA. However, need for strengthening the local parts ecosystem.

Hyundai/Kia: Only ~35% of sales are U.S.-built. 65% of vehicles sold in the U.S. are imported from outside North America. Very low domestic parts content (~13%). High tariff risk.

Volkswagen: Only ~21% of U.S. sales are domestically assembled. 36% are from overseas, 43% from Mexico/Canada. Even U.S.-built models rely heavily on imported components.

BMW: ~60% of U.S. sales are built in Spartanburg, SC, mostly SUVs. Remaining ~40% are imports (mostly sedans). However, engines/transmissions are imported from Europe—even in U.S.-built vehicles.

Mercedes-Benz: ~30% of U.S. sales are assembled in Alabama. 70% are imports (many from Germany). Even U.S.-built SUVs use German engines and transmissions. High exposure.

Used Car Market Surge: As new vehicle prices rise, consumers are expected to delay purchases—boosting demand for used cars and parts. Expect aftermarket players (AutoZone, O’Reilly, etc.) to benefit.

Industry Realignment Ahead: Tariffs will accelerate M&A, new factory announcements, and strategic shifts in sourcing and production. Automakers with idle U.S. capacity or localization-ready platforms will move fast to adapt.

Strategic Takeaways for Boards

Reevaluate Exposure: Map vehicle and parts sourcing against tariff risk—prioritize high-volume SKUs.

Accelerate Localization: Move beyond final assembly; localize powertrains, batteries, electronics.

Adjust Portfolio: Prioritize domestically built models in sales and marketing; phase down high-risk imports.

Double Down on Messaging: Emphasize “American-made” credentials with dealers, consumers, and regulators.

Looking Ahead

The tariff regime marks a fundamental break from three decades of global auto supply chain norms. In the short term, the U.S. auto market will contract. Over time, the winners will be those who can pivot fast, build local, and pass through minimal price shocks.

In this trade war, scale, speed, and supply chain localization will separate winners from losers.

Help Shape the Next Memo

We’re building BoardMemos for people like you—boardroom decision-makers, strategists, and executive teams.

What company, sector, or trend do you want us to decode next?

Tell us here 10 secs FILL-OUT form

We share 2-3 briefings each month: sharp, executive-ready, no decks, no fluff.

BoardMemos

Boardroom-ready insights. No decks. Just decisions.